Treasury Management and Investment Strategy 2022/23 - 2025/26

By: Director, Finance and Corporate Services

To: Audit and Governance Committee - 25 November 2021

Subject: Treasury Management and Investment Strategy 2022/23 - 2025/26

Classification: Unrestricted

For Decision

Summary

The CIPFA Code of Practice on Treasury Management and the CIPFA Prudential Code require the Authority to determine and set the Treasury Management Strategy for the financial year ahead as part of the annual budget papers in February of each year. Part of the Terms of Reference of the Audit and Governance Committee is to review the Treasury Management Strategy and Investment Strategy and agree the draft in principle prior to it being presented to the full Authority in February each year as part of the suite of budget papers.

The capital figures detailed within the draft strategy provide a current estimate of forecast spend but maybe subject to refinement prior to the February Authority meeting, as projects progress or slip as more detailed work in costing and profiling is undertaken, to ensure affordability.

The Authority continues to prioritise security and liquidity over potential yield in line with CIPFA guidance, whilst ensuring that the treasury activity undertaken complies with the agreed strategy.

Recommendation

Members are requested to:

1. Review and agree in principle, the Treasury Management and Investment Strategy for 2022/23 (paragraphs 9 to 59 refer).

Lead/Contact Officer: Finance Manager – Nicola Walker

Telephone Number: 01622 692121 ext. 6122

Email: Nicola.walker@kent.fire-uk.org

Background Papers: Treasury Management Strategy 2020/21

Annual Treasury Management and Investment Strategy 2022/23

Introduction

1. Treasury management is defined by the Chartered Institute of Public Finance and Accountancy’s (CIPFA) Treasury Management Code of Practice as: “the management of the Authority’s borrowings, investments and cash flows, its banking, money market and capital market transactions; the effective control of risks associated with

those activities; and the pursuit of optimum performance consistent with those risks”.

2. There are two parts to the treasury management operations, the first is to ensure that the Authority’s cash flow is adequately planned, with cash being available when it is needed. Surplus monies are placed in low-risk counterparties or instruments in line with the Authority’s low risk appetite, providing adequate liquidity initially before considering investment return. The second main function of treasury management is the funding of the Authority’s capital plans. The Capital Strategy provides a guide to the borrowing need of the Authority, essentially the longer-term cash flow planning to ensure that the Authority can meet its capital spending obligations.

3. The CIPFA Code of Practice on Treasury Management (TM) and the CIPFA Prudential Code require local authorities to determine and set the Authority’s Treasury Management Strategy, its Strategy relating to investment activity, and Prudential Indicators on an annual basis. The Authority currently has cash backed reserves and balances of circa £42m, so it is important that robust and appropriate processes are in place to ensure adequate security of the sums invested, as a loss of principal will in effect result in a loss to the General Fund. Set out below are the key elements of the Strategy covering the borrowing requirements and investment arrangements.

4. The Authority’s Investment Strategy has regard to the TM Code and the Guidance. It has two objectives: the first is security, in order to ensure that the capital sum is protected from loss, ensuring that the Authority’s money is returned; and the second is portfolio liquidity, in order to ensure that cash is available when needed. Only when the proper levels of security and liquidity have been determined can the Authority then consider the yield that can be

obtained within these parameters.

5. This Strategy has been created based on the CIPFA 2017 Prudential and Treasury Management Codes, which requires the Authority to prepare a Capital Strategy. The Capital Strategy is a document in its own right which is being reported separately to the Authority in February as part of the budget papers. This Authority does not envisage any commercial investments and has no non-treasury investments.

Policy Statement

6. The Authority regards the successful identification, monitoring and control of risk to be the main criteria by which the effectiveness of its treasury management activities will be measured. Accordingly, the analysis and reporting of treasury management activities will focus on their risk implications for the organisation.

7. The Authority acknowledges that effective treasury management will provide support towards the achievement of its business and service objectives including its Customer and Corporate Plan and long term Capital Strategy. It is therefore committed to the principles of achieving value for money in treasury management and to employing suitable comprehensive performance measurements, within the context of effective risk management.

National Guidance and Governance

8. This Strategy complies with the CIPFA Treasury Management in Public Services Code of Practice and Cross-Sectoral Guidance Notes (“the TM Code”), and Guidance on Local Government Investments issued by the Secretary of State for Communities and Local Government under section 15(1)(a) of the Local Government Act 2003 (“the Guidance”). Specific decisions on the timing and amount of any borrowing will be made by the Authority’s

Director, Finance and Corporate Services in line with the agreed Strategy.

9. Governance: The Audit and Governance Committee is required to receive and approve a number of financial reports each year, which cover the following:

(a) An Annual Treasury Management and Investment Strategy: This Strategy forms part of the February 2022 budget report to Authority. This Strategy therefore includes:-

- the Capital Programme together with the appropriate prudential indicators;

- the minimum revenue provision (MRP) policy, which details how residual capital expenditure is charged to revenue over time;

- the Treasury Management Strategy, which defines not only how the investments and borrowings are to be organised, but also sets out the appropriate treasury indicators; and

- an Investment Strategy which sets out the parameters on how deposits are to be managed.

(b) A Mid-year Treasury Management Report: This will usually be presented to Members of Audit and Governance in the autumn and provides an update on the Capital Programme, amending prudential indicators and/or the Strategy, if necessary;

(c) A Year-end Annual Report: This provides the final outturn position for the year in relation to investments and deposits made during the year, prudential and treasury indicators, and a summary of the actual treasury activity during the year.

External Support

10. Treasury Management Advisor: The Authority uses Link Group (previously known as Capita Asset Services) as its external Treasury Management Advisor. The Authority recognises that the responsibility for treasury management decisions remains with itself and will ensure that undue reliance is not placed upon the external advisor. The current contract has recently been renewed with Link Group and expires at the end of September 2024.

11. Administration: Day to day treasury management activity, such as placing deposits in institutions, is carried out on behalf of the Authority by the Kent County Council Treasury and Investment Section under a Service Level Agreement, which is reviewed on a regular basis.

The Capital Prudential Indicators 2022/23-2025/26 and the Minimum Revenue Provision (MRP) Statement

12. The Authority’s capital expenditure plans are the key driver of treasury management activity. The output of the Capital/Infrastructure Plan is reflected in the Prudential Indicators, which are designed to assist Members’ overview and confirm capital expenditure plans.

13. Capital Expenditure: This can be funded from a variety of sources such as directly from the revenue budget, capital receipts (money received for the sale of the Authority’s assets) capital grants or from borrowing. The Authority’s Capital Plan, and the revenue and capital resources being used to finance it, are shown in Table 1 below. Where there is a difference between planned expenditure and cash resources, this will result in an increase in the net financing need and hence the potential need to consider external borrowing. The Authority will only ever borrow to fund capital expenditure. Given that interest rates remain at an all-time low, it may be prudent at some stage to consider whether there is a need to borrow to fund future elements of the capital programme. However, despite low interest rates in recent years, this has not been necessary in the last 10 years. The capital figures detailed below

provide a current estimate of forecast spend but maybe subject to refinement prior to the February Authority meeting as projects progress or slip as more detailed work in costing and profiling is undertaken, to ensure affordability.

Table 1 - Capital Expenditure

| Capital Expenditure | 2021/22 Forecast (£'000) | 2022/23 Estimate (£'000) | 2023/24 Estimate (£'000) | 2024/25 Estimate (£'000) | 2025/24 Estimate (£'000) |

|---|---|---|---|---|---|

| Total Capital Expenditure | 5,104 | 20,293 | 6,748 | 6,428 | 6,519 |

| Funded By Revenue / Infrastructure funding | -5,104 | -13,393 | -4,048 | -4,744 | -3,519 |

| Funded By Capital Receipts | 0 | -6,900 | -2,700 | -1,684 | 0 |

| Net Financing Need (Borrowing) for the Year | 0 | 0 | 0 | 0 | 3,000 |

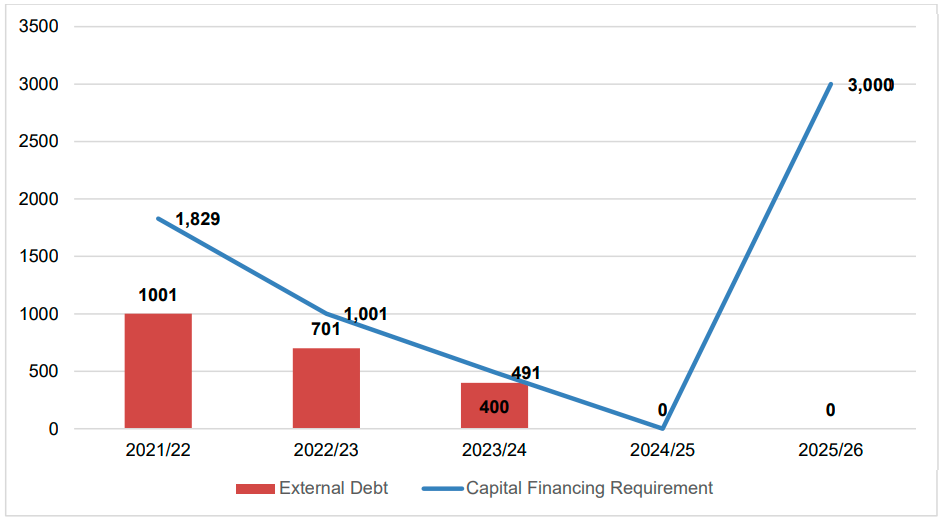

14. The Authority’s Borrowing Need [the Capital Financing Requirement (CFR)]: The CFR is the total historic outstanding capital expenditure which has not yet been paid for from either revenue or capital resources. It is essentially a measure of the Authority’s indebtedness and its underlying borrowing need. Any capital expenditure above, which has not immediately been paid for through revenue or capital resource will increase the CFR. The CFR projections are shown in Table 2.

Table 2

| Capital Financing Requirement |

2021/22 Forecast (£'000) | 2022/23 Estimate (£'000) | 2023/24 Estimate (£'000) | 2024/25 Estimate (£'000) | 2025/26 Estimate (£'000) |

|---|---|---|---|---|---|

| Opening CFR | 2,798 | 1,829 | 1,001 | 491 | 0 |

| Movement in CFR | -969 | -828 | -510 | -491 | 3,000 |

| Closing CFR | 1,829 | 1,001 | 491 | 0 | 0 |

| Movement in CFR represented Net Financing Need (Borrowing) for the Year | 0 | 0 | 0 | 0 | 3,000 |

| Movement in CFR represented Less: Provision for Principal (MRP/VRP)* | -969 | -828 | -510 | -491 | 0 |

| Movement in CFR | -969 | -828 | -510 | -491 | 3,000 |

*The CFR does not increase indefinitely, as the minimum revenue provision (MRP) is a statutory annual revenue charge which reduces the indebtedness in line with each asset’s life.

Capital Financing Requirement Profile vs External Debt Profile (year-end position)

15. Core Funds and Expected Investment Balances: The application of resources (capital receipts, reserves, etc.) to finance capital expenditure or other budget decisions to support the revenue budget will have an ongoing impact on investments/deposits. Detailed below in Table 3 are estimates of the year-end balances for each cash-backed resource, working

15. Core Funds and Expected Investment Balances: The application of resources (capital receipts, reserves, etc.) to finance capital expenditure or other budget decisions to support the revenue budget will have an ongoing impact on investments/deposits. Detailed below in Table 3 are estimates of the year-end balances for each cash-backed resource, working

balances and the net amount of capital expenditure funded from internal resources

(historical under-borrowing). The sum of these balances is the amount estimated as

available for investment.

16. Working balances comprise of the estimated net difference between amounts owed to or

by the Authority (debtors and creditors and other amounts paid or received but not yet

charged to the accounts). The amount under-borrowed in this table relates to historical

capital expenditure that was identified as needing to be funded from borrowing in earlier

years, but where a decision was made to use internal cash balances instead of external

debt (this is shown calculated in Table 2 above), less the actual amount of external debt at

the end of each year. Table 6 further below details how the under-borrowing is then

calculated.